Fund Scan: IDG Ventures India makes hay out of rising share of rupee capital

VC Circle

March 6, 2018

IDG Ventures India’s fundraising experience for its first two funds is a study in contrast. But with its third fund, the venture capital firm appeared to have found a balance as it turned to rupee capital. The move was in stark contrast to the way most of its peers raised money, but exits remained a worry, mirroring the industry story.

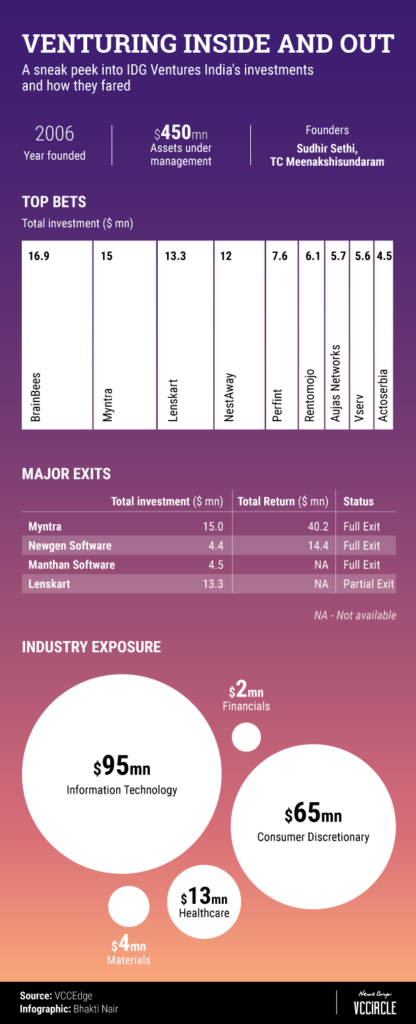

The journey, which dates back to 2006, saw IDG Ventures India co-founder and chairman Sudhir Sethi looking to raise a $100-million early-stage venture capital fund.

To begin with, the going was good. On 21 May, Sethi was scheduled to meet IDG Inc. founder and chairman, the late Patrick McGovern, at Bengaluru’s Oberoi Hotel for about half an hour. The discussions, however, went on well beyond two hours, and subsequently spilled over to the next few days. The conversations on the telephone resulted in a four-page plan by Sethi. McGovern went through it in details and, finally on 21 June, suggested that the VC firm should look at raising a $150-million fund instead of the planned $100 million.

“Pat (McGovern) also said that he was keen to anchor the fund and commit the entire $150 million,” said Sethi, who had, by then, roped in his “buddy” TC Meenakshisundaram as the second co-founder. The third, Manik Arora, moved out of the firm in 2015, and Sethi had little to share about his role.

The founders pressed on the gas to meet the 1 September, 2006, launch target and built a robust team around them. By the time the fund marked the final close at $150 million in February 2007, it had a host of other foreign players joining in as limited partners, besides IDG Inc.

Fast forward to 2012-13, IDG Ventures India hit the streets to raise its $175-million second fund, according to a filing with the Securities and Exchange Commission (SEC). The situation, however, was starkly different.

According to Sethi, the VC firm had initially set out to raise a “sizable fund“, but finally had to settle for just about $95 million. The poor macro environment and absence of a showcase exit were the root cause, he said.

Sethi and Meenakshisundaram realised that a change in strategy was the way forward, and shifted their focus to domestic investors. This, at a time when most of its global and homegrown peers were still dependent on foreign institutions and individuals to raise capital.

With the third fund, IDG Ventures India met the targeted fund size of $200 million comfortably with domestic LPs contributing significantly to the fund.

“IDG definitely has set an example among VCs to raise rupee capital. Of course, because of confidentiality issues, it would be difficult to examine each and every VC fund to find their (respective) domestic LP share base,” said an industry veteran.

The trigger

The strategic shift towards domestic investors was, however, not easy. After nearly three months of scanning the domestic market, the broad feedback was “not to waste time, as domestic investors were not ready to take the plunge on such long-term assets”.

But the founders were not in a mood to relent, despite the fact that some of its peers, such as Nexus Venture Partners, Matrix Partners and Kalaari Capital, formerly IndoUS Venture Partners, continued to raise sizeable amounts for their new funds.

Though IDG Inc. continued to anchor the funds with significant commitment, the pressure to expand the investor base was growing, Sethi added. But despite the odds, there were a few positive signals in the domestic market as Sethi’s team continued to meet domestic investors.

Finally, discussions with over 100 family offices started reaping the results with the rupee ratio of its funds slowly growing from about 20% to breach the 40% mark in the past five years.

Today, IDG Ventures India counts Infosys co-founder Kris Gopalakrishnan, Asian Paints Family Office and Small Industries Development Bank of India as its limited partners.

“Not only have they raised rupee capital, but they have been able to raise nearly 50% of their exits in rupee money, too. I think both the factors validate the coming of age of the domestic economy in the VC market,” the industry expert cited above said. He was referring to a string of exits IDG Ventures India made in the past two-and-a-half years.

“I think, we need people who are focused on India. IDG is an exemplar of venture capital funds and new domestic firms should be guided by its model,” he added.

Another fund manager was of the view that the capital should come from the domestic market, especially in a country like India, which is resourceful enough. International money should only be a top-up, he added.

The fund manager’s views were reflected in yet another industry insider. VC firms have been forced to take international money because the culture of turning to domestic investors barely existed. But with the local market developing, not only are domestic LPs have deeper understanding of the market, they can also co-invest with it, he added.

Besides, local capital is an important and significant element to drive confidence for international capital to flow world over, explained Sethi.

Focus on technology

IDG Ventures India was the only venture capital player to have a 100% focus on technology right from the very outset, unlike most of its peers, which moved between tech and non-tech businesses, as the internet and mobile market was not considered deep enough a decade back.

The full bias towards technology could, however, be attributed to the background of the founders. Sethi has spent his career spanning 35 years in the technology sector, starting with software services firm HCL and Wipro, where he met Meenakshisundaram 25 years ago.

Sethi’s appointment as the country head of Walden International in 1998 marked his entry into the venture capital world. He led investments in IT major Mindtree Consulting and Venture Infotek in the fintech space, among others. Meenakshisundaram was also part of the investments. Arora, the third co-founder, had experience in the sector while working as an investor in General Atlantic and Battery Ventures.

IDG Ventures India’s first investment was in business intelligence and analytics company Manthan Software Services Pvt. Ltd. It was also a first mover in the medical-tech space with Perfint Healthcare and was among the first investors in the ecommerce space with its investment in fashion e-tailer Myntra, which was later acquired by ecommerce giant Flipkart.

The venture capital firm, which has made over 70 investments across its three funds, invests broadly in four sectors – consumer media and technology, software products and software-as-a-service sector, besides fintech and health-tech. “Our focus has remained consistent, while the underlying sub segments have evolved over the years,” said Sethi.

Strategic shifts

While IDG Ventures India has been a technology-focussed VC firm over the past 11 years, its investment strategy based on sector and stage choices has evolved over the years.

From being a pure play early-stage investor with its first fund, the focus has is now more nuanced. The VC firm allocates 10% to seed stage investments and 25% to expansion stage deals, while the bulk, or 65% of the funds, make investments at Series A and Series B levels.

“This nuanced strategy allows the team to create early distributions to investors, while also backing promising teams very early in the life cycle. The DNA of the team is to enter early and to be thesis-driven,” said Sethi.

With its strategy to allocate funds at the expansion stage, the VC firm has also been able to garner quick exits. Its most recent exit from Newgen Technologies through its initial public offering (IPO) is a case in point.

In terms of sectors, IDG Ventures India has added several fintech companies to its third fund portfolio, which includes online lending platform EarlySalary. As part of its expansion stage funding in the fintech space, the VC firm’s notable investment is in online insurance selling platform Policybazaar.

As part of its overall deal scouting strategy, IDG Ventures India draws out a sound thesis. As part of its ecommerce investment strategy, it has backed Myntra, online eyewear store Lenskart and online shopping store for kids and baby products FirstCry. The firm’s sharing economy strategy finds resonance with its investments in home rental startup NestAway, online rental marketplace for furniture and other home appliances Rentomojo, and on-demand fashion rental platform FlyRobe.

“Sethi is willing to see deals that does not fit into western textbooks,” the industry expert cited above said.

IDG Ventures India has also built a strong co-investment programme with its investors to drive deeper engagement in the startup space. For instance, the innovation programme with Unilever Ventures is a partnership to scan the market and back promising ideas. “Once they grow, they could be potential investment or acquisition targets for our LPs,” said Sethi.

Exits

IDG Ventures India has made 14 exits in the past two and a half years, and many are in the pipeline, said Sethi, but did not specify the kind of returns the VC firm has made or are expecting from its future deals.

“Credentials and track record are built on exits and not investments alone. It is important to engineer and create liquidity with discipline and strategy,” said Sethi, adding that 50% of all exits have been made to Indian buyers.

IDG Ventures India has made significant money when Flipkart acquired Myntra, and when Newgen went public in India and Yatra was listed on the NASDAQ. It has also marked several secondary exits through partnership with larger PE players.

Other exits made through the mergers and acquisitions route include mobile apps and proprietary products developer Sourcebits, cloud-based web and mobile app security testing provider iViZ Techno Solutions; and home services startup Zimmber, according to VCCEdge, the data and research platform of News Corp VCCircle.

The VC firm has also exited Flipkart, after picking up a stake in the ecommerce major during the Myntra deal.

Exits through secondary deals also include Manthan, when Singapore’s state-owned investment firm Temasek led a $60 million investment round in the Bengaluru-based firm in 2015. The VC firm also partially exited Lenskart, after PremjiInvest, the family office of IT czar and Wipro chairman Azim Premji, invested in the firm in 2016.

The firm roughly made Rs 94 crore, or an internal rate of return of 28-30% during its exit from Newgen, according to VCCircle estimates. In comparison, private equity and venture capital firms typically chase an IRR of 20-30%.

The venture capital industry, too, have seen a chunk of exits during the period, although comparisons are difficult given that VC firms do not make the figures public.

However, compared to its peers, the startups backed by IDG appeared to have suffered less casualty. “There will be many startups that fail to raise capital or create a meaningful business model, and subsequently shut down. Failure is not a bad word in the startup world, rather fail fast and learn fast is the goal,” said Sethi. Education portal iProf Learning, which was part of IDG’s portfolio, was one such startup to shut shop.

Team play

Though Arora left IDG Ventures India in 2015 for reasons not know, it is not the only VC firm to have witnessed key executives leaving. Matrix Partners saw its co-founder leaving to start his own firm. SAIF Partners has also seen two executives parting ways to launch their own funds. Kalaari Capital, Sequoia and Helion Venture Partners, too, have seen co-founders and senior executives moving out.

However, IDG Ventures India is known to groom in-house talent and make leaders of them.

“TCM (Meenakshisundaram) and I started off with three key focus areas – sharing of responsibilities, ownership and sharing of economics,” said Sethi, adding that the firm has built a strong set of leaders – Karan Mohla, head, Delhi and Northern Region and sector head for Consumer; Karthik Prabhakar, global head for fundraising; Venkatesh Peddi, sector head for software; Ranjith Menon, sector head for health-tech; and Sanat Rao, the head for seed investments.

Prabhakar, in fact, had joined the firm as a summer intern and went on to become a partner in five years. We are currently grooming our next set of high-performing leaders, he added.

India expertise

IDG Ventures India will remain focused on how to build a value-added venture firm with a strong exit culture and deep India-expertise.

“We are executing a vision on being an expert on India. We will continue to back Indian entrepreneurs. We will continue to have 75% of the capital going to solving challenges faced by India.”

Sethi said he is also optimistic about the future given that it is an opportunities galore in the technology space. In the first quarter in 2006, the team had evaluated 67 deals, now we look at 600-plus deals every quarter, he said.

What remains interesting, however, is whether the share of rupee capital in IDG Ventures India’s funds continues to grow in subsequent rounds of fund raising.